Like many people who work to keep us safe, firefighters and members of the Fire Service face an increased risk to their well-being every day just to do their jobs.

- Although firefighters work in a field that poses increased risks to their safety, they can secure life insurance policies that fit their lifestyle and budget.

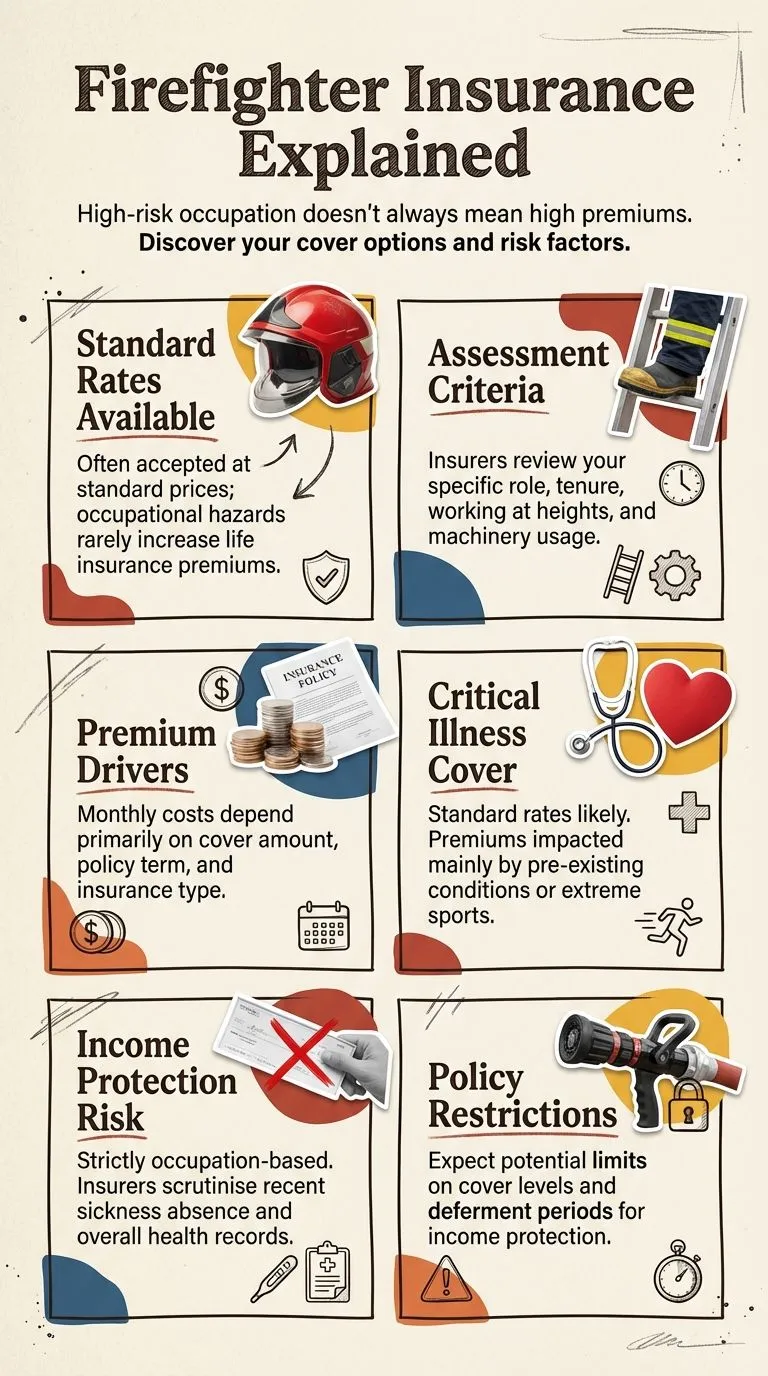

- In most cases, applications for life insurance for firefighters are accepted at standard terms and with standard monthly premium payments.

- The application process is often straightforward, as no family or personal medical disclosures are usually required.

UK Fire Service Life Cover From Claybrooke – Quick Quote Form

The Perceived Risk

Since this profession carries a higher risk than others, many people believe that securing a life insurance policy may be more difficult and, if they can secure one, it will be much more expensive in terms of monthly premium payments.

The good news is that this is not always the case. Here, we will discuss what you should know.

Critical Illness Cover for Firefighters

Like a life insurance policy, critical illness cover is generally easy to apply for and secure.

Providers often do not view the firefighting profession as an increased risk of an individual contracting a critical illness, so they are usually accepted at standard terms and with standard monthly payments.

Click To Compare QuotesAlthough this is true of critical illness cover, it is important to note that the Total and Permanent Disability option is not available for firemen at this time, but is a small part of the overall policy.

Income Protection for Firefighters

Income protection policies are available at standard terms and rates for firefighters, depending on the insurance provider.

When submitting the application, it is important to choose the “own occupation” option to secure the best possible policy with standard terms.

This means a claim against the policy will be assessed on the individual’s ability to work as a firefighter.

Own occupation is the most straightforward definition to claim against compared to the other available definitions.

Other available definitions for income protection include “any occupation” and “suited occupation.”

These definitions mean that when a claim is filed, it will be assessed based on the individual’s ability to perform a similar job or any job.

While these definitions can be valuable, they are much harder to place a claim against, making the occupation definition option the best choice for those in the firefighting occupation.

If you need more information on these definitions, you can contact Claybrooke.

The deferment period for an income protection policy for firefighters is often set in increments ranging from 1 day to 52 weeks.

This deferment period is the time that lapses between the individual stopping work, placing the claim, and the claim being paid.

When choosing a deferment option, consider the other benefits you may receive from your employer, how much financial support you will need while out of work, and your current savings.