Life Insurance underwriting implications for people with rheumatoid arthritis

When considering applications for rheumatoid arthritis life insurance protection, critical illness (CI) cover, and disability benefits, underwriters aim to gather as much information from clients at the outset of their condition.

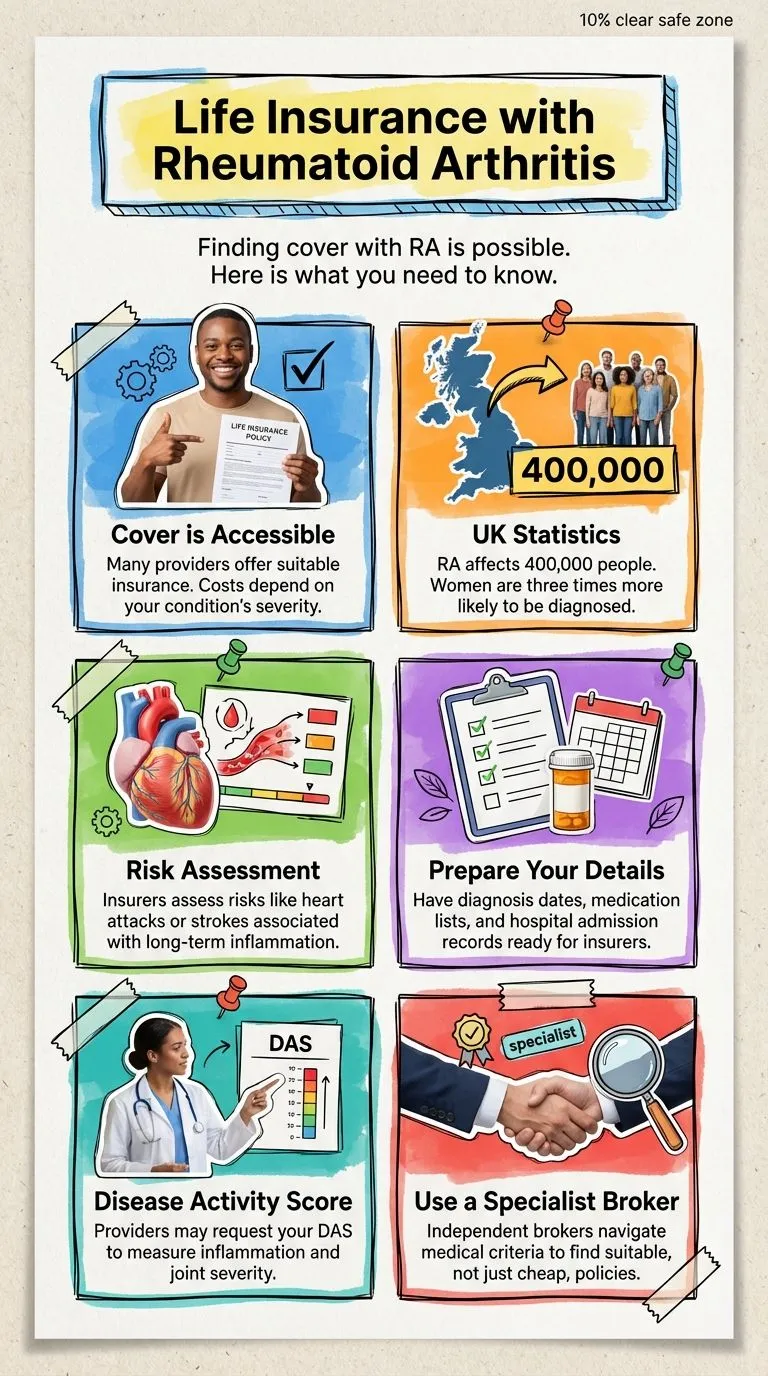

The severity of the disease can be evaluated based on the extent of the symptoms, treatment, and level of handicap.

In the mildest cases, terms-for-life cover, critical illness, and disability benefits may be offered without further specific medical proof of illness.

A general practitioner’s report is required for more moderate to severe cases.

In their report, underwriters look to establish the disease’s pattern, the severity of symptoms, any blood test or x-ray results, the facts of any prescribed treatment, and any complications.

Specialist Life Cover From Claybrooke – Quick Quote Form

The disease’s severity can be categorised as one of the following:

Mild -slight pain and stiffness in the peripheral joints, minimal swelling, and no deformities.

RF is negative, and ESR and CRP are normal. No erosions were found on X-rays, and the patient can perform all normal daily activities.

Moderate -difficult pain, major joint involvement, or movement constraint in affected joints.

The patient requires frequent and continuous drug therapy. RF is positive, and ESR or CRP is slightly increased. The patient can perform all facets of daily life with slight difficulty.

Severe -chronic, active disease, with no release from pain and also severe restriction of movement and impairment of function.

RF is positive, and ESR or CRP is significantly increased. The patient’s daily life activities are restricted and may require physical assistance.

For mild cases, underwriters may offer life at ordinary rates or at a lower rate, and exclude RA from CI and disability benefits.

For moderate cases, life cover, CI, and disability benefits may be rated at 75 per cent, with an RA exclusion for CI and disability benefits.

Click To Compare QuotesUnderwriters can only offer life cover with a minimum rating of +100 per cent for severe cases.

Additional ratings also apply to ongoing steroid treatment or additional cardiovascular risks.

Rheumatoid arthritis can make normal daily activities incredibly challenging

Claybrooke talks about symptoms, treatment, and underwriting implications

There are many different types of arthritis—inflammatory and degenerative, for example.

However, Rheumatoid Arthritis (RA) is inflammatory and progressive in nature, and it is also the result of an autoimmune disorder.

This means the body’s immune system, which produces antibodies to destroy viruses and foreign bacteria, mistakes its tissue as foreign and fires antibodies to attack it, causing inflammation.

With RA, inflammation primarily occurs at the joints’ linings and can affect virtually any joint in the body, depending on the case.

Symptoms most often occur first in peripheral joints, such as the hands, feet, and wrists, presenting as fluctuating pain, weakness, and stiffness, or a feeling of stiffness in the morning.

Many also find that RA gives them flu-like symptoms or makes them feel tired, agitated, or depressed.

Due to the nature of RA, the symptoms will likely come and go. Relapses of symptoms are known as ‘flare-ups’ and are caused by increased blood flow to the area around the joint.

The joints become red, warm, and painful as fluid gathers around them and the ligaments are forced to stretch.

As the condition progresses, cartilage protecting the ends of the bones starts to thin, which can lead to possible bone erosion.

Eventually, bone erosion leads to loss of movement and joint shape, and the joint will ultimately need to be replaced.

Without a good treatment response, disabling joint destruction can occur quickly.

Varying Degrees

The level of handicap varies and depends on the aggressiveness of each case.

In milder cases, only peripheral joints are affected; however, in more progressive cases, RA can spread to more major joints, such as the shoulders, elbows, and hips.

The disease’s course cannot be predicted, but generally follows the more progressive tract.

Periods of remission are common after the first appearance of symptoms, but after two or three relapses, a chronic form of the condition is likely to set in.

Click To Compare QuotesRA is not just a disease of joint degeneration–because of its auto-immune nature, RA can cause inflammation in any part of the body.

This type of inflammation is known as an extra-articular disorder (not limited to the joint).

In more serious cases of RA, inflammation can appear in the following locations:

Skin. Damage to the blood vessels is called vasculitis, and these vasculitic lesions can cause skin ulcers.

Heart. A collection of fluid around the heart from inflammation is not uncommon.

Although this typically causes only mild symptoms, they can be severe. Inflammation can affect the heart muscle, valves, and blood vessels.

Lungs. The lungs can be affected in two ways:(1) fluid can collect around one or both lungs, or (2) tissues in the lungs may become stiff or overgrown. Both forms of inflammation can hurt breathing.

Eyes. The eyes usually become dry, inflamed, or possibly both, and this type of inflammation is called Sjogren syndrome.

The severity of this condition depends on the part of the eye affected.

RA is not fatal on its own, but life expectancy is shorter than that of the general population for those with the disease due to the extra-articular complications and the side effects of treatment.

Extra-articular complications increase with occurrences of ischaemic heart disease and stroke in those with RA.

RA can be hard to diagnose due to the many other conditions that cause joint pain, and also a lack of a definitive diagnostic test to distinguish RA from the rest.

A diagnosis of RA is based on the body’s symptoms and supported by blood test results.

One test is for the Rheumatoid Factor (RF) antibody in the blood. RF is positive in about 80 percent of RA patients.

However, RF also tests positive in around 5 per cent of people without RA; therefore, further tests are necessary.

Other common tests used to support an RA diagnosis include the following:

Erythrocyte sedimentation rate (ESR). This test detects inflammation in the body, indicating the disease’s activity.

C-reactive protein test (CRP). This test also indicates inflammation and RA activity.

Full blood count (FBC): About 80 percent of RA patients develop anaemia, a decrease in red blood cells that, when anaemic, cannot carry oxygen to the brain. This test also provides strong support.

X-rays. These check for physical changes in joint structure throughout the body.

Common Treatments

To treat RA symptoms, doctors can prescribe anti-inflammatory drugs, which reduce pain and swelling but do not slow down joint damage.

During relapse flare-ups or in more severe cases, immunosuppressants or oral steroids may be necessary, though these, too, have their complications.

Click To Compare QuotesImmunosuppressants bring the immune system back to a normal state but can also reduce the response to infections.

Oral steroids, such as prednisone, reduce pain and swelling and also slow joint damage, but they can only be used for a short time.

Steroids become less effective the longer they are used, and long-term use can cause bone thinning, cataracts, raised blood pressure, and diabetes.

Facts and Figures

- RA affects more than 350,000 people in the UK.

- The cause of RA is unknown, and it can occur at any age (most common between 30 and 50).

- Females are three times more likely to receive an RA diagnosis compared to males.

- Smoking increases the risk of RA, especially in non-menopausal women.

- RA is more common than leukaemia and multiple sclerosis.

In general, people with RA:

(1) 20% have very mild symptoms.

(2) 75% continue to have flare-ups.

(3) 50% of RA patients cannot work ten years after onset.

(4) Around 10-20 per cent of affected persons deteriorate to the point of being wheelchair-bound or bedridden.