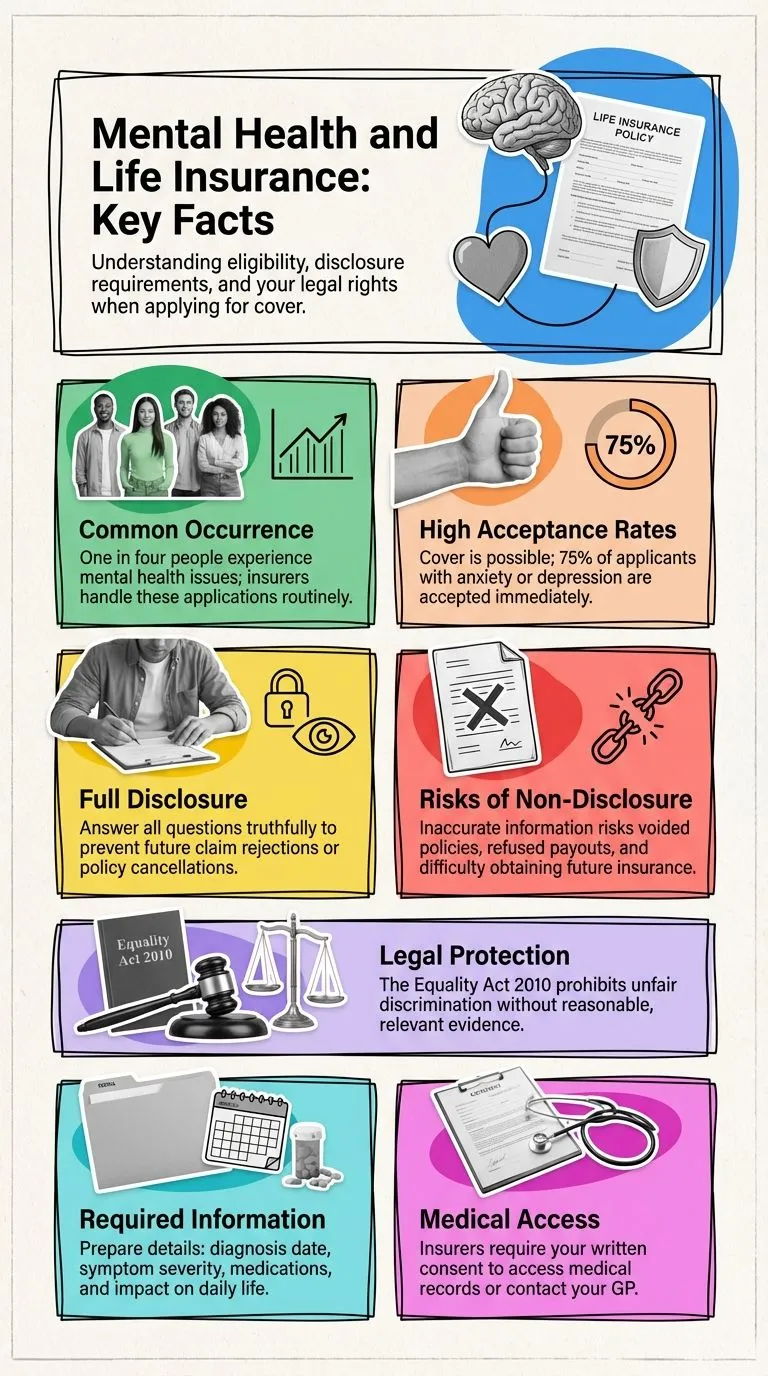

Mental health can sometimes affect life insurance cover, and the extent of the condition and its recentness often determine the outcome.

More specifically, a past condition has far less impact on life insurance than a current condition.

A condition with recurring, severe symptoms will have a greater impact than one with less severe daily symptoms.

The good thing is that many medical conditions still allow individuals to obtain life insurance to protect their debts or families.

Depending on the circumstances and after being subject to the underwriting process, it is possible to get life insurance while having anxiety, depression, stress, bipolar disorder, panic attacks, and incidents of self-harm and suicide attempts.

Life Cover From Claybrooke – Quick Quote Form

Life Insurance with a History of Anxiety

Depending on which insurer you choose, applicants with anxiety may be refused life insurance by one insurer when they otherwise would qualify with another insurer.

On a similar note, certain insurers will “rate load” your monthly premiums higher than others, so even if you are declared eligible for cover, it may still not be your best possible price.

Hence, it is important to get the best advice.

Those with a history of anxiety may be required to answer additional questions to begin the underwriting process for your application with the insurer’s underwriters.

Immediate action could be taken and decisions made quickly.

Click To Compare QuotesStill, if you have any complications or other related conditions, the underwriters likely have to contact your general practitioner to investigate further.

In addition to the standard medical questions, the underwriters will have more specific questions to ask as well to paint the clearest picture for your application:

- If you have ongoing symptoms

- Details of severe attacks or symptoms and the dates

- Details of time away from work in the past 12 months

- Details and dates of any treatment, medication, or therapy

- Details of any suicide attempts or self-harm

- Details and dates of hospital admissions

- Details regarding general health

- Details of alcohol/drug consumption

Depression and Life Insurance

We are regularly asked about how depression relates to life insurance, considering that depression is one of the most common forms of mental distress for applicants over the age of 35.

The monthly premiums are similar to those of anxiety when ratings and loadings are applied, though some insurers treat the condition differently and therefore need different information.

Even if you have been declined life insurance in the past because of depression, there may still be an insurer out there for you.

There are equally those who reject such applications and others who offer more flexibility and understanding.

That is why getting sound advice is necessary to ensure you get the best possible level of cover for the right price.

Cost of Life Insurance with Anxiety, Depression, or Stress

Life insurance rates for anxiety, depression, and bipolar disorder are often the same as those of unaffected applicants and, therefore, can be offered ordinary rates.

Click To Compare QuotesCosts can be higher for certain applicants when compared to applicants without a more detailed medical history, but you can minimise these increased rates if you go to the right insurer.

Some insurers might rate load premiums by 50-100 per cent depending on the outcome of their underwriting process.

Life Insurance for Bipolar Disorder

As is the case with life insurance and other mental health conditions, bipolar disorder can surely affect your application.

For example, bipolar disorder will likely receive a slightly higher rate of premium loading than an incident of general, life-related stress or anxiety, as bipolar disorder is considered a more chronic or specified condition.

Critical Illness Insurance with Mental Health Issues

Critical illness insurance for individuals with a history of mental health concerns is usually applied for and processed in the same way as regular life insurance.

Based on the statistics, the main difference is that critical illnesses are much more likely to be diagnosed, so the underwriting process can be far more thorough, with more specific questions and information requested.

Policy premiums can increase by a larger percentage, and in cases of severe mental health concerns, critical illness coverage may be declined, while life-only protection may be accepted.

Some cases are more acceptable for critical illness coverage than others, depending on the date, severity, and treatment: (1) anxiety, (2) depression, (3) stress, (4) bipolar disorder, (5) panic attacks, (6) after self-harm, (7) after a suicide attempt.